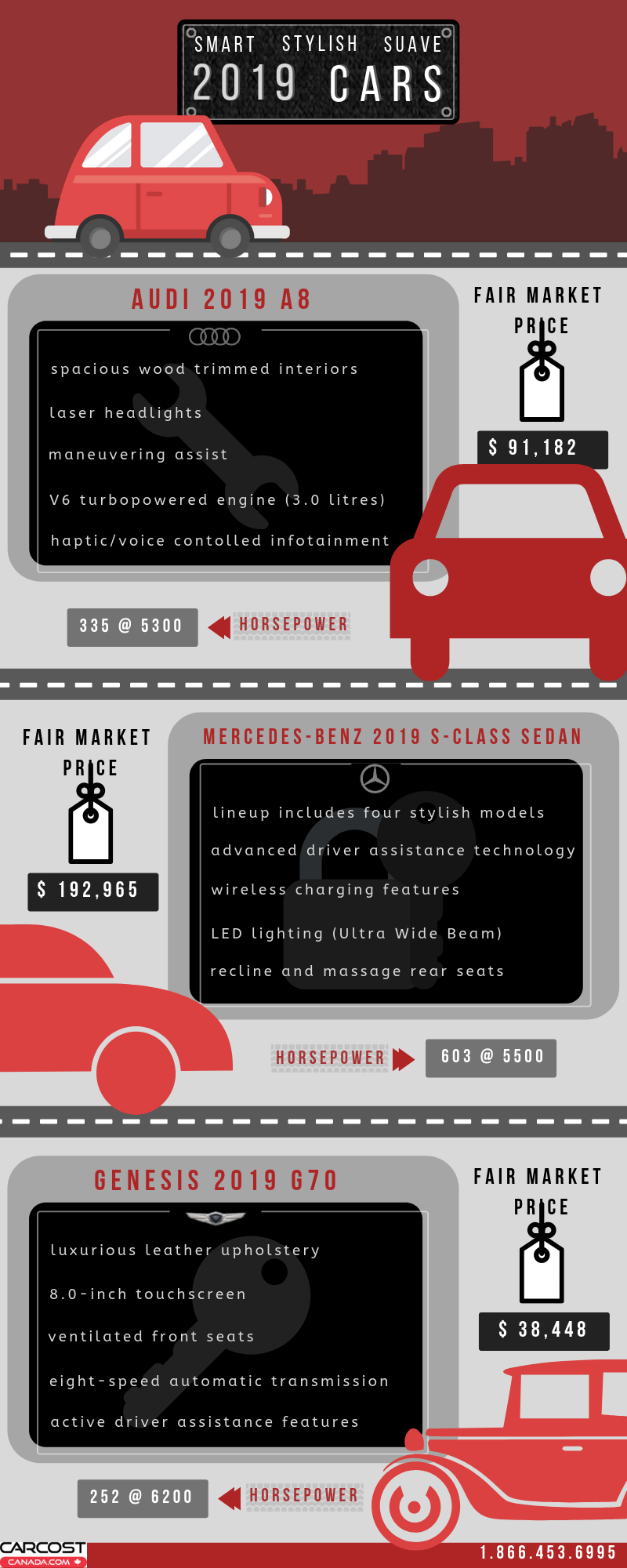

Buying a new car is such an exciting experience. But wait, it isn’t just about cruising down to your local dealership and picking out your next ride. The first step? Budgeting! The main hitch that most novice car buyers face is that they assume the price instead of actually crunching the numbers.

Naturally, this leads to spending more than bargained for. To avoid this scenario and make sure your next car fits seamlessly into the budget, it’s important to know the dealer invoice price in Canada. Moreover, let’s say you’re shopping for an Acura, Car Cost Canada can help you access great rebates and incentives, and save you the hassle of negotiation.

Without further ado, let’s explore 5 tips to ensure that you don’t break the bank with your next ride!

- Calculate Your Monthly Expenses

Before delving into your new car purchase, gather your most recent credit card statements; mortgage, utility, cell, and internet bills. Bifurcate all monthly expenses into two sections; fixed and variable. The former should include those that involve a flat unwavering figure; rent, whereas the latter includes items like your grocery bills that change from one month to the next.

- Take Into Account Your Disposable Income

From your monthly income subtract your total expenses. Then decide how much of this figure is disposable and how much you want to put away for a rainy day. A great rule of thumb is to not spend over 10% of your household income on a single-vehicle. In the end, the amount you splurge on your car wholly depends on the breadth of your other expenses.

- Familiarize Yourself With Ownership Costs

There’s a difference between how much you can spend and how much you should spend. Car ownership fees include insurance, financing, maintenance, fuel, and depreciation. This can roughly amount to $790 every month.

The biggest strain on your wallet will be depreciation. In fact, it is estimated that a car depreciates by as high as 30% the moment you drive it off the lot. Fuel, interest, and insurance follow close on the heels of this expense. Once you’ve tabulated ownership costs, it’ll be easy to narrow down your options to cars that can stay within budget.

- Consider Future Costs

If you’re looking at a long car loan, remember that your financial situation in the future will be somewhat constrained. Take into account other expenses like rent that may increase in the future, making it tricky for you to afford your car payments. Since this can divert your budget in a big way, it’s best to factor them into your current disposable income.

- Get a Free Dealer Invoice Report

The last and final step is to get a free dealer invoice report. Your report will reveal;

- MSRP (Manufacturer’s Suggested Retail Price – what the dealer paid to own the car)

- Factory incentives

- Lease and finance rates

- Recommended dealerships

- Vehicle pricing options

- Comparable vehicles

A majority of dealers turn a profit of 8.7% on selling a new car. When you’re aware of the true MSRP, you can follow the 3-5% rule – meaning you can add about 3-5% on the invoice figure in your report to calculate the most lucrative negotiation price.

It’s simple! Choose your make and model and see a complete breakdown of all fees.

Get a FREE dealer invoice report in your email within minutes.